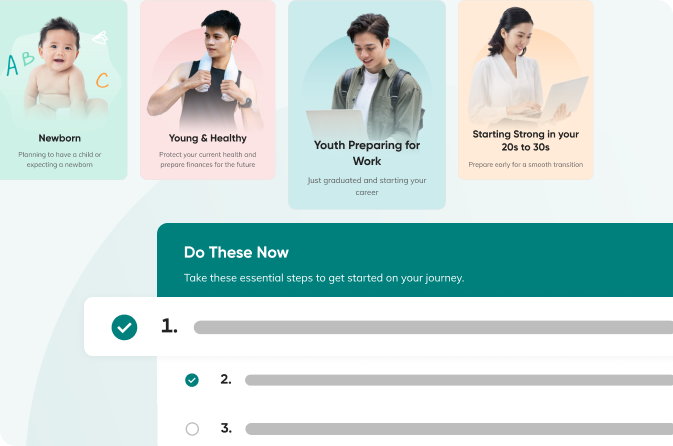

Essential tips to navigate major life stages

Insurance Solutions for your life stage

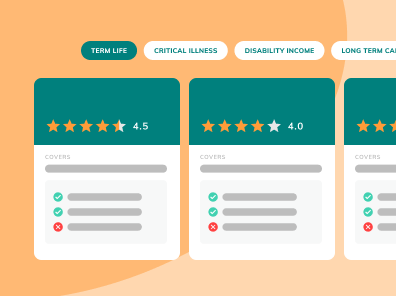

First-of-its kind insurance plan rating & commentary

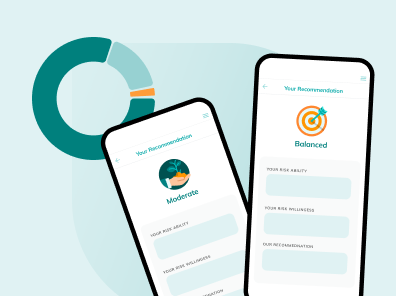

Investment Solutions for your goals

Breaking down life’s financial curiosities

Comprehensive guidance and principles

Want to plan for a home, build an emergency fund, or set savings goals? Our calculators help you do the math, so you get clear answers for smarter financial decisions.

Comprehensive checklists and essential financial tips curated to guide you through key life stages.

Explore our tailored solution sets crafted to meet your financial needs,from insurance product reviews and curated packages to investment solutions.

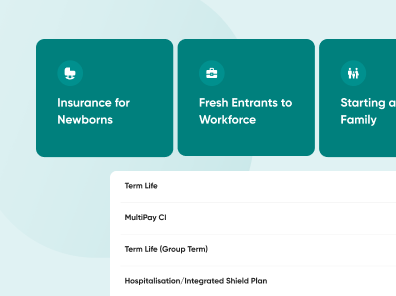

Curated insurance product sets for core protection needs for your life stage

First-of-its-kind insurance product rating and assessment

Cost-effective, global investment funds to enable your life goals

Gain practical tips and insights on key financial topics, including:

We partner companies, unions and community associations to uplift the wellbeing of employees and member through financial literacy programmes, mostly free of charge.

What the CareShield Life Changes Mean for Singaporeans (August 2025)

Beyond Tax Incentives: Rethinking Financial Planning for the Everyday Person

Insurance Jargon Decoded: What Pre-Authorisation Really Means for Your Hospital Coverage

Financial Advice is not a Substitute for Financial Literacy

Rising Private Hospital Bills Are Stretching Insurance – and Your Wallet

")