By Chuin Ting Weber, CFP, CFA, CAIA

CEO & Chief Investment Officer, MoneyOwl

Place no store by what the banks’ spokespeople say that this is not a problem.

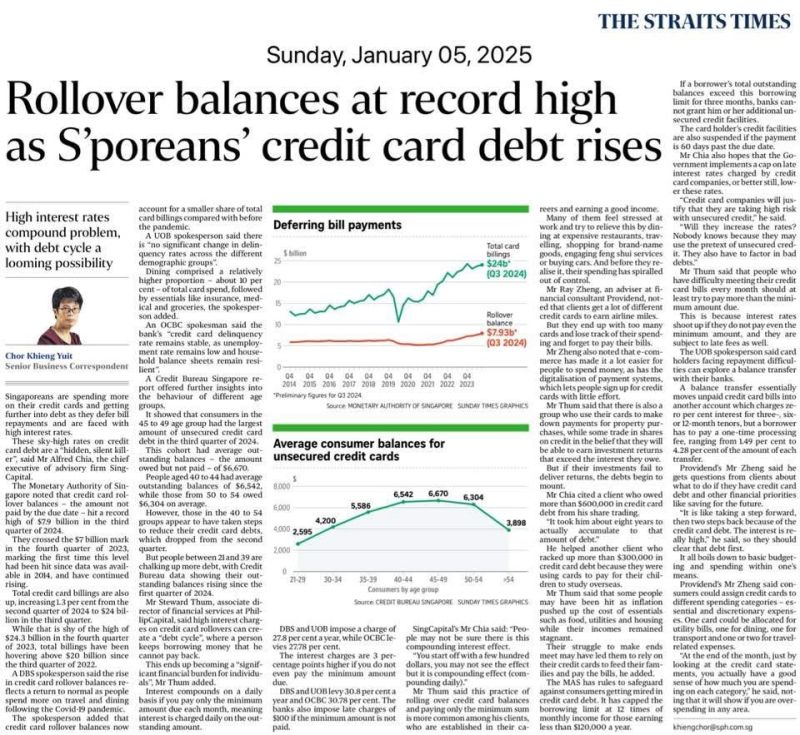

Delinquency not being a problem is a bank measure, not a citizen well-being metric.

The best mass market customer for the bank is exactly the one who would roll over balances and pay 30% p.a.

That interest rate means that almost one in three can default without the bank losing money.

This is core to the business model of banks.

High interest unsecured consumer debt for the mas market is one of the worst traps of modern capitalism, & the common prudential wisdom is not to regulate the sky-high rates.

Not worth arguing about this for now – let’s just help ourselves. The bank is not wired to help you.

Please know also, that you cannot turn to the other offerings of the bank – to “invest” your cashflow – to get out of this. Can’t make a quick buck that way.

(I keep a non-privilege account, so I get all the mass market calls. In fact, one of the worst practices to me is banks offering a loan on a credit card at lower rates to help me take advantage of investment opportunities! Read “speculation”.)

If you’re in credit card debt, know that it is possible to get back into financial health. I’ve actually been there and done that myself, a few decades ago. It might take quite some years but it gets easier after a certain point (because interest on lower balances is lower, so there’s a reverse of the compounding effect) and there are tools and programmes available.

No shame to taking action to course correct.

Let’s take care of ourselves and one another: family members, colleagues.

Perhaps start by checking out a rubric we wrote on MoneyOwl’s website on reducing debt.

Subscribe here for our soon-to-come and free OwlHoots on financial planning insights and analysis.

Disclaimer:

While every reasonable care is taken to ensure the accuracy of information provided, no responsibility can be accepted for any loss or inconvenience caused by any error or omission. The information and opinions expressed herein are made in good faith and are based on sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. The author and publisher shall have no liability for any loss or expense whatsoever relating to investment decisions made by the reader.