Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

Some people think that it is not necessary to buy life insurance, Ironically, insurance and investments are really two sides of the same coin in building your wealth.

Why should I pay to be protected from something that is not likely to happen and with the money I can’t get back? They may think it is better to accept the risk and retain full control over their money instead of depending on someone else’s terms and conditions.

For these people, if something happens to them, they plan to depend on their savings and investments to tide them through. And if nothing happens, it would be as if their bet won out, and they didn’t have to spend a single cent on insurance.

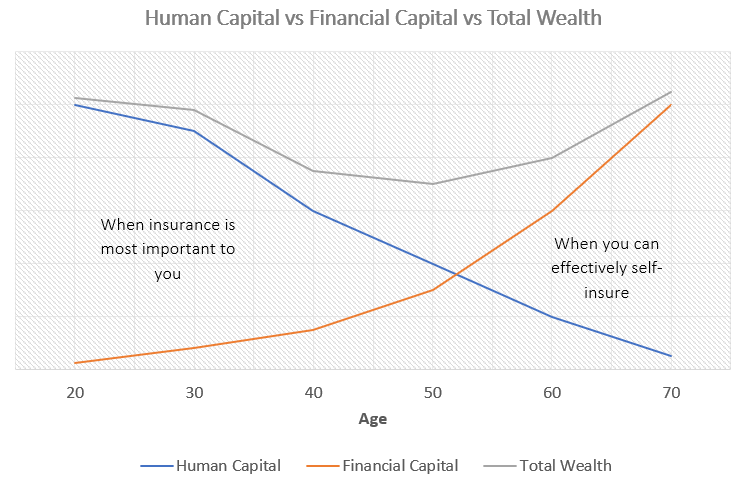

Ironically, insurance and investments are really two sides of the same coin in building your wealth. When you are in your 20s, your human capital (i.e. present value of future earnings) is most substantial. Your financial capital which refers to your savings and investments will be at its lowest since you have just started earning.

Should you suddenly lose your ability to earn, you will find yourself with a substantial drop in your total wealth which you now have no way to replace. No matter how good you are at investing, there is no way the additional returns you can get from saving on insurance can beat the lump sum returns from an insurance payout.

What’s more, most investments need time to compound and grow exponentially while riding out short term market volatility. If you cash out on your investments prematurely, you may end up losing your capital, which is a double whammy to you in times of need.

On the other hand, if you’re much older in your 50s to 60s, you would have already accumulated sizeable financial capital. With your human capital at its lowest, it may make more sense to depend on your investments to tide you through any mishaps, than to start buying insurance at this point which is likely going to be very expensive. In such a situation, where your wealth is more than able to replace your future income, you can effectively self-insure. Life insurance is less important to you at this stage.

This chart shows how your human capital (and hence the importance of insurance) and financial capital change throughout your life.

At MoneyOwl, we strongly encourage our clients to be adequately covered before we recommend them to start their wealth accumulation journey. A well-designed insurance plan ensures that it protects you on your path to building wealth. It is like having a spare tyre in your boot. Should one of your tyres get punctured, it isn’t game over for you. With a replacement tyre, you can continue your journey to your destination with as minimal disruption as possible.

Don’t wait until your tyres get punctured then start scrambling to find a replacement. Start your insurance journey with us today!

This is a MoneyOwl exclusive series. Read the rest of the insurance principles: