Note: It was announced in November 2023 that MoneyOwl will be acquired by Temasek Trust to serve communities under a re-purposed model, and will move away from direct sale of financial products. The article is retained with original information relevant as at the date of the article only, and any mention of products or promotions is retained for reference purposes only.

______________

What are Investment Linked Policies (ILPs)?

ILPs are made up of an insurance component coupled with investment funds managed by professional fund managers. Insurers usually offer a limited number of sub-funds for each ILP with differing investment objectives to suit the risk appetite of policyholders. The allocation of premiums across these sub-funds may be fixed by the insurer or decided by the policyholder, depending on the structure of the ILP. The premiums you pay are used to pay for insurance charges and to buy investment units. Also, to pay for the various policy fees and charges, some investment units will need to be sold.

Key features of ILPs include flexibility & the potential for higher return. For example, you could change your investments by switching sub-funds, topping up your investments, taking a premium holiday or making partial withdrawals without affecting your insurance coverage. You could also adjust your insurance coverage as your life stage changes. As you are investing in more aggressively managed funds, surrender values may be potentially higher compared to traditional whole life plans whose funds (also called Participating Funds) are managed more conservatively by the insurer.

On the other hand, the criticisms of ILPs include its high fees and charges, long lock-in periods, disappointing investment returns, and a limited number of funds as these are pre-selected by the insurer. However, insurers have been increasing their fund offerings over the years.

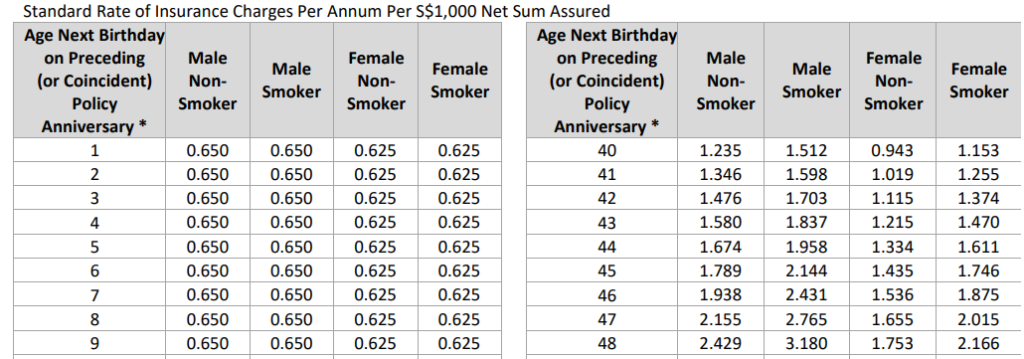

Another overlooked aspect of ILPs is that as the policyholder gets older, the cost of insurance will go up (see example below). This means more investment units will be sold to maintain your insurance coverage, leaving less invested units to potentially earn investment returns. The insurance policy may also terminate if there are insufficient units to pay for policy charges. This could be due to several reasons such as poor performing funds, frequent or large partial withdrawals, or failure to pay premiums regularly.

Example of cost of insurance in an ILP taken from an actual Policy Illustration

Is it time to review my Investment Linked Policy?

It is always a useful practice to review your overall insurance needs at least once a year or whenever you are about to enter a new stage of life. For existing ILP policyholders who contact us for help, they often do so after hearing about the ‘perils’ of owning an ILP from their well-meaning friends and family. There are also certain social media groups that suggest ILPs are ‘scams’ to void. Thus, it is understandable to feel conflicted about whether such a policy remains a good fit for you.

Should I remain on the policy, switch, or adjust it? And what better options are out there?

These are some common questions from our client conversations. As a conflict-free financial advisory, MoneyOwl follows a consistent set of advisory processes & planning philosophies to provide our clients with clarity and confidence in addressing if an ILP is still suitable.

Here, we summarise our approach to how an ILP policyholder may maximise its effectiveness and benefits, particularly in terms of customisation and control based on individual needs.

A Three-Step Process for Assessing your ILP

Step 1: Determine Insurance Gaps and Flexibility of Coverage

To evaluating whether an ILP is still suitable for you, it is crucial to assess the adequacy of your insurance coverage needs holistically. Avoid just looking at the protection component of your ILP in isolation.

At MoneyOwl, depending on your personal circumstances such as family size, income source and amount of personal cash savings, we have a framework of the recommended amount of insurance coverage to protect yourself and your family members in cases of death, total and permanent disability, as well as critical illness. Life-stage changes, such as marriage, the birth of a child (or more), or changing financial responsibilities, can impact the level of coverage needed.

We then review clients’ existing policies to help them identify potential gaps to ascertain whether their ILP aligns with their overall insurance needs. This also involves taking into account the current health condition of the client. We know that ILPs may allow for adjustments in insurance coverage but we need to understand the specific terms and conditions of the ILP in question. Some ILPs may include additional charges should there be a change within the first 5-10 years of the policy.

Step 2: Evaluate Investment Needs, Performance and Control

One of the key attractions of ILPs is the investment component. This allows policyholders to achieve potentially higher returns in allocating premiums to their chosen investment sub-funds. This contrasts with traditional whole-life plans, where the investment strategy is determined by the participating funds of insurers and may not align with an individual’s risk appetite and financial goals.

But jumping into evaluating the investment performance alone is not recommended in silo. We need to help clients to know the purpose and the need for investing based on their circumstance and to uncover the expectations and investment personality or risk profile of the client.

Only then do we proceed to evaluate the performance of the chosen sub-funds linked to the ILP. We look into historical performance, asset allocation strategies, and fund management fees. For example, comparing the ILP’s investment performance with alternative global benchmarks can help determine if the ILP offers a competitive return on investment. In the end, clients would have a clearer view of how the investment component of the ILP may fit into their investment strategy.

Step 3: Putting it together according to one’s financial plan

At this point, with a better understanding of their insurance and investments needs, we can proceed to consider the ILP’s place in the overall financial plan. Most clients would, by now, have made a decision to keep, change or terminate their ILPs. For example, if there is a large insurance gap and clients are not able to afford additional premiums, they may decide that it is more urgent to terminate their ILP and channel the premiums to purchase a low-cost term insurance. However, it may be that the client is not able to purchase new insurance due to pre-existing conditions and will be forced to retain the ILP for protection. For another example, if the client has enough insurance coverage and is confident that the sub-funds will continue to perform, he may want to continue the ILP but reduce the insurance component to increase the investment component.

What else do I need to know when continuing with my ILP?

Assessing the suitability of an ILP for the long-term isn’t straightforward. We also need to consider how the escalating mortality (risk associated with death) & morbidity (risk associated with critical illness) charges may increase with age. Depending on the terms and conditions, some newer ILPs will only charge when the total protection coverage is less than the investment value of the policy. However, some ILPs, which are predominantly for protection, may provide an insurance coverage on top of the investment value. For example, when an ILP provides a $200,000 death cover but after 15 years, it only manages to accumulate $130,000 in investment returns, then there will be insurance charges imposed through the sale of sub-fund units to cover the difference (also called the sum-at-risk). This means that understanding the long-term cost implications of mortality and morbidity charges and their impact on the overall value of the policy is crucial.

Always remember that when you buy an ILP, it’s your responsibility to choose and keep an eye on the sub-funds. Some clients relied solely on their insurance agents’ initial sub-fund selection recommendations and neglected to monitor the performance for years. Eventually, they were dissatisfied with the underperforming funds and upset that their agents had ‘disappeared’. To effectively manage an ILP in the long run, you must be actively involved and have the time to consistently monitor its performance. Since insurance agents’ competency can vary, policyholders must adopt a proactive approach and monitor their ILP’s investment performance instead of leaving it to chance.

Conclusion

While there are ways to navigate the policy term and adapt an ILP to one’s changing life needs, it is crucial to recognise that ILPs may not be suitable for everyone. One must therefore carefully evaluate their financial goals, risk tolerance, sufficiency of coverage, and most importantly, their willingness and commitment to actively manage their investments over time.

By adopting a straightforward and cost-effective approach, individuals can navigate the complexities of insurance and investments with confidence, aligning their financial strategies with their goals and priorities. This will allow individuals to allocate more time and energy to other important aspects of life, such as nurturing meaningful interpersonal relationships and gaining valuable life experiences!

Disclaimer:

The information contained herein does not have any regard to the specific investment objective(s), financial situation, or the particular needs of any person. Buying insurance is a long-term commitment and should be bought according to your needs, and products’ suitability. You may wish to seek advice from our client adviser before making any financial decision.