Navigate Parenthood with Confidence

Comprehensive checklists to help you prepare for every stage from newborns to students covering education, tuition, medical insurance, and more, so you can focus on what matters most.

Skip the queue and get the convenience by booking home-based vaccination service with telehealth providers.

Craft your Will using MoneyOwl’s Digital Will-Writing service

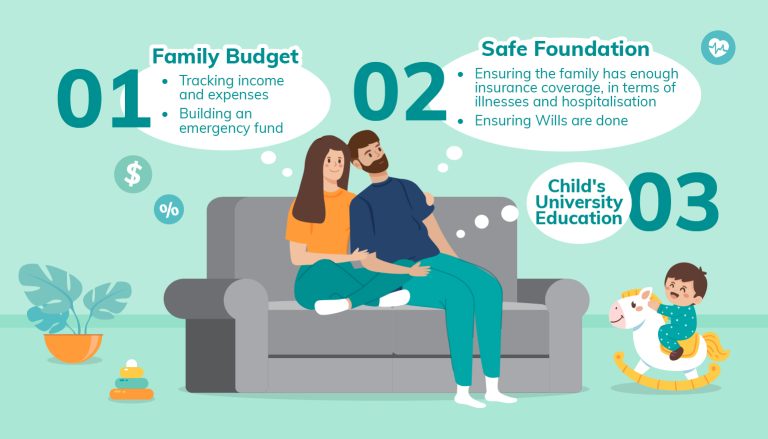

This e-book demonstrates how to optimise government grants, the types of insurance needed for adequate protection, how to grow your money so you can plan for your child’s education (and your retirement) as well as how to plan for all those big what-if scenarios.

Skip the queue and get the convenience by booking home-based vaccination service with telehealth providers.

Craft your Will using MoneyOwl’s Digital Will-Writing service

This e-book demonstrates how to optimise government grants, the types of insurance needed for adequate protection, how to grow your money so you can plan for your child’s education (and your retirement) as well as how to plan for all those big what-if scenarios.

Craft your Will using MoneyOwl’s Digital Will-Writing service

This e-book demonstrates how to optimise government grants, the types of insurance needed for adequate protection, how to grow your money so you can plan for your child’s education (and your retirement) as well as how to plan for all those big what-if scenarios.